Remittance

5 Best Payment Gateway Services Built for Global Growth

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Stablecoins are becoming the remittance standard because they enable always-on, verifiable cross-border settlement when paired with strong infrastructure.

Remittance is one of the last corners of global finance where “modern” still means business hours, multiple intermediaries, and settlement timelines that are hard to explain to customers.

Money leaves one country. It disappears into the system. Days later, it shows up somewhere else. Sometimes. Eventually?

For years, that slowness was treated as inevitable. Cross-border money movement was just assumed to be expensive, opaque, and delayed. Operators built support teams and pricing models around those constraints instead of questioning them.

That’s starting to change.

Stablecoins are quietly becoming the default settlement rail in more remittance flows, not because the world suddenly fell in love with crypto, but because operators are tired of paying for delays, FX opacity, and support tickets they can’t answer cleanly.

The standard is shifting for a very practical reason: stablecoins remove the slowest, least predictable part of remittance (cross-border settlement) without forcing teams to rebuild everything else.

The rail that becomes the standard is the one teams default to when optimizing for cost, speed, availability, and reliability. It’s the option operators reach for when they want fewer exceptions, fewer tickets, and fewer surprises.

That’s what’s happening with stablecoins in remittance. In many corridors, they’ve reached the point where they are simply the cleanest settlement option available.

You see this most clearly in high-fee corridors where traditional rails stack costs at every hop. You see it in weekend and after-hours transfers, where bank cutoffs introduce artificial delays. You see it in recipient behavior: people prefer holding dollars, or at least value stability over local-currency volatility.

In regards to the U.S., 26% of these remittance users have already used stablecoins for international transfers. It’s evident that stablecoins aren’t an experiment; they’re becoming the default.

Most remittance products aren’t slow because of pay-in. They’re slow because of what happens after.

Cross-border remittances still rely on chains of intermediaries, each with their own batch windows, cutoffs, and reconciliation processes. When something stalls, it’s often unclear where the money is or who owns the delay.

That opacity shows up immediately in operations. Support teams can’t give precise answers. Finance teams can’t predict availability confidently. Product teams hesitate to promise faster delivery because the system can’t reliably back it up.

This drag isn’t abstract. It turns into higher fees, longer “where is my money?” loops, and corridor expansion that takes months instead of weeks.

As of early 2025, the global average cost to send $200 using traditional remittance methods is still over 6 percent, more than double the UN’s stated goal of 3 percent, according to data from the World Bank. That gap exists largely because settlement remains slow and layered with intermediaries.

A sender pays in using a card or bank transfer. Behind the scenes, that value is converted into a stablecoin, often without the sender needing to think about crypto at all.

From the user’s perspective, they sent money. From the system’s perspective, value has been moved into a rail that can travel globally without waiting on bank settlement windows.

The stablecoin transfer happens on-chain. This is where finality matters.

Instead of waiting for multiple institutions to reconcile balances, the transfer reaches confirmation instantly through atomic settlement and cryptographic finality — no T+2 reconciliation, no intermediary queues. There is a concrete reference that operators can track, log, and verify.

For support and operations, this is a big shift. "In motion" becomes observable instead of inferred.

On the receiving side, the stablecoin is converted back into local value through an off-ramp. That might mean a bank deposit, mobile money credit, wallet balance, or cash pickup, depending on the corridor.

This step matters more than the chain itself. If off-ramps are slow, expensive, or unreliable, the product fails no matter how fast the transfer leg is.

One of the underappreciated benefits of stablecoin settlement is reconciliation clarity.

An on-chain reference combined with a clean internal transaction model reduces ambiguity during disputes, investigations, and audits. Operators can answer what happened without stitching together reports from five systems.

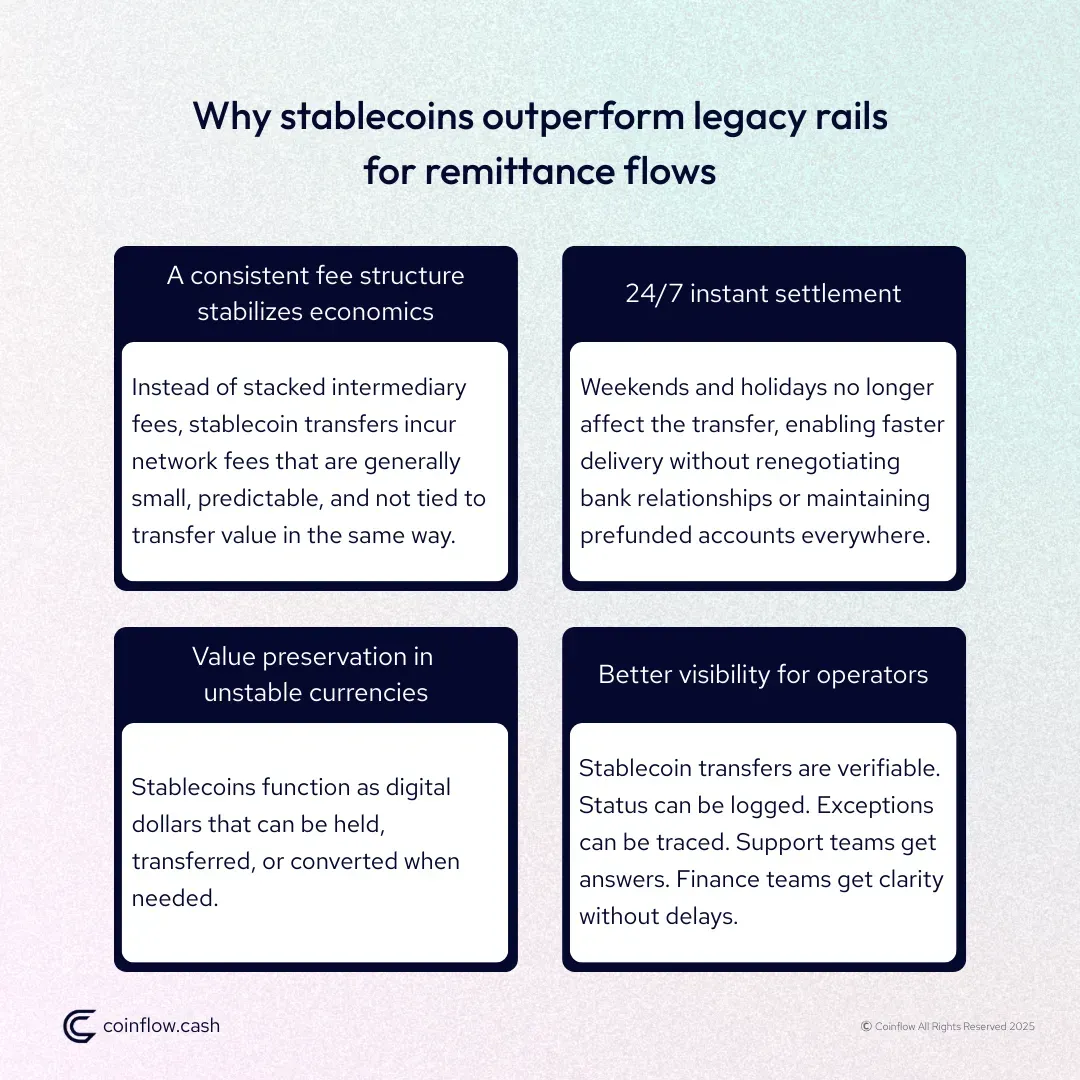

Instead of stacked intermediary fees, stablecoin transfers incur network fees that are generally small, predictable, and not tied to the transfer value.

In high-volume corridors like the U.S. to Mexico or parts of Africa, this can reduce costs dramatically. In some cases, fees drop to a fraction of a percent, changing the economics of the product entirely.

Weekends and holidays no longer matter for the transfer leg. That alone removes a huge source of user frustration and operational complexity.

For remittance providers, this means faster delivery without the need to renegotiate bank relationships or maintain prefunded accounts worldwide.

In many recipient markets, users actively want exposure to their money. Stablecoins function as digital dollars that can be held, transferred, or converted when needed.

Perhaps the biggest operational win is visibility.

Stablecoin transfers can be verified. Status can be logged. Exceptions can be traced. Support teams get answers instead of guesses. Finance teams get clarity instead of delays.

KYC, AML, sanctions screening, and transaction monitoring still apply. In some cases, the bar is higher, not lower.

Any remittance operation using stablecoins needs compliance controls that are built into the flow, not bolted on later.

Users don’t care how fast the transfer leg is if cash-out is confusing or unreliable.

Local payout partners, pricing transparency, and availability matter more than on-chain speed alone.

Wallet UX, recovery flows, scam prevention, and support readiness all shape whether users feel comfortable using the product again.

Thin liquidity can erase cost advantages quickly. Stablecoin settlement works best when liquidity is actively managed and matched to corridor demand.

Unify IDs across pay-in, conversion, transfer, and payout. Normalize statuses. Establish a clear event trail.

Deploy stablecoins where they reduce time-to-available funds and support load. Keep traditional rails where they perform better.

Transaction screening, thresholds, and audit-ready logs should be native to the system, not external add-ons.

Clear payout options, transparent fees, and predictable outcomes matter more than raw speed.

The goal isn’t replacement, it’s intelligent routing.

When stablecoin settlement is implemented well, the impact shows up quickly. Fee pressure eases without sacrificing margin. New corridors launch faster. Fewer transfers disappear into black boxes. Settlement becomes something teams can predict, explain, and scale with confidence as volume grows.

That’s why stablecoins are becoming the standard. Not everywhere, and not all at once, but wherever speed, cost, and visibility actually matter to the business.

What’s becoming clear, though, is that stablecoins only deliver this upside when they’re part of a coherent operating model. On their own, they don’t fix fragmented pay-ins, brittle payout flows, compliance gaps, or poor visibility. The teams seeing real gains are the ones treating stablecoins as infrastructure inside a broader, well-designed money movement system.

Coinflow is built for remittance teams that want stablecoin settlement without turning their stack into a patchwork. By unifying pay-ins, stablecoin and fiat settlement, payouts, compliance controls, and end-to-end visibility in one platform, Coinflow removes the fragmentation that slows teams down and creates blind spots as complexity increases.

Stablecoins are treated for what they are: infrastructure. A practical way to move money faster across borders while keeping operations verifiable, controlled, and compliant. The result is a remittance stack that settles faster, is self-explanatory, and scales without increasing risk or operational overhead.

If you want to see what stablecoin settlement looks like when it’s built into a production-grade remittance system, talk to our team. We’ll walk through your corridors, constraints, and goals, and show how Coinflow helps teams adopt stablecoins as part of a multi-rail strategy.

Daniel is the CEO and Co-Founder at Coinflow, connecting traditional payment rails with stablecoin technology to enable instant global settlement for trusted, cross-border commerce.

Remittance

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Remittance

Hidden FX markups, multi-day settlement, and opaque correspondent banking chains erode remittance margins. See how modern FX payment infrastructure eliminates each one.

Fintech

Real-time payments are projected to hit 22% of global transaction volume by 2028. Here's how marketplaces, e-commerce, gaming, payroll, remittance, and fintech platforms are using instant settlement to drive real business outcomes.