Remittance

5 Best Payment Gateway Services Built for Global Growth

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Legacy payments slow teams down. Our guide explains how to modernize pay-ins, payouts, and settlement without rebuilding your entire stack.

Most companies don’t struggle with payments because they picked the “wrong” provider. They struggle because the system they’re using was designed for a version of the business that no longer exists.

Modernizing payment infrastructure isn’t about chasing shiny technology. It’s about removing structural friction in how money moves so your product can ship faster, settle faster, and clearly explain what happened when something inevitably goes sideways.

This is where stablecoins often get misunderstood. They aren’t the product, they’re the key infrastructure. And that’s exactly why they matter. Used correctly, they compress settlement time, simplify cross-border movement, and make money movement easier to verify. Not louder. Just cleaner.

When people talk about modernizing payments, they usually mean “our processor.”

That definition is too narrow to be useful.

Payment infrastructure is the full system responsible for how money enters your product, moves through it, and leaves it again, along with the controls and visibility needed to operate that system safely at scale.

Modernization isn’t one upgrade. It’s aligning all of these layers around faster, safer, and more explainable money movement.

Most payment stacks weren’t designed to be “bad.” They were designed around assumptions that no longer hold.

Legacy assumptions that create modern pain.

Many systems still assume batch windows and business hours in a world that operates 24/7. The core issue is architectural: legacy rails separate the message layer from the value layer, and that gap is where settlement delays, opaque fees, and reconciliation headaches originate. Settlement cutoffs that made sense for banks don't map cleanly to global digital products.

Fragmentation is another culprit. Pay-ins, payouts, risk tooling, and reporting often live with different providers. Each one is optimized for its own job, but none of them share a unified view of the transaction lifecycle.

Settlement is frequently opaque. Money is “in motion,” but teams can’t confidently answer where it is, when it will land, or what’s blocking it.

Exceptions scale faster than teams do. As volume grows, edge cases turn into daily work instead of rare events.

And feature delivery becomes tied to vendor roadmaps instead of your own. When adding a new flow means waiting on multiple providers, innovation slows down fast.

These architectural issues don’t stay contained in finance or ops.

None of this shows up as a line item on a pricing page, but it compounds quietly over time.

Payments don’t stop at 5 p.m. Infrastructure can’t either. Modern systems are designed to operate continuously, not around cutoff times that only make sense on paper.

Modern stacks support multiple rails cleanly: cards, bank transfers, real-time rails where available, international methods, and stablecoin settlement as another tool—not a special case.

The difference is whether those rails share a consistent operating model or introduce more fragmentation.

Tokenization shouldn’t stop at checkout. Any stored credential tied to payouts, recurring flows, or long-lived accounts needs the same protection. Modern systems minimize where sensitive data exists at all.

A modern payments system can answer simple but critical questions:

If those answers require stitching together reports from multiple tools, observability is missing.

Modernization should happen in phases. But modular adoption can’t turn into a vendor maze. The system needs flexibility without sacrificing coherence.

Stablecoins tend to attract extreme reactions. Either they’re dismissed entirely or treated as a cure-all.

Both are wrong.

At their best, stablecoins are infrastructure. They offer faster settlement windows, global movement with fewer intermediaries, and clearer auditability depending on implementation.

They don’t replace your payments stack. They improve one part of it: settlement.

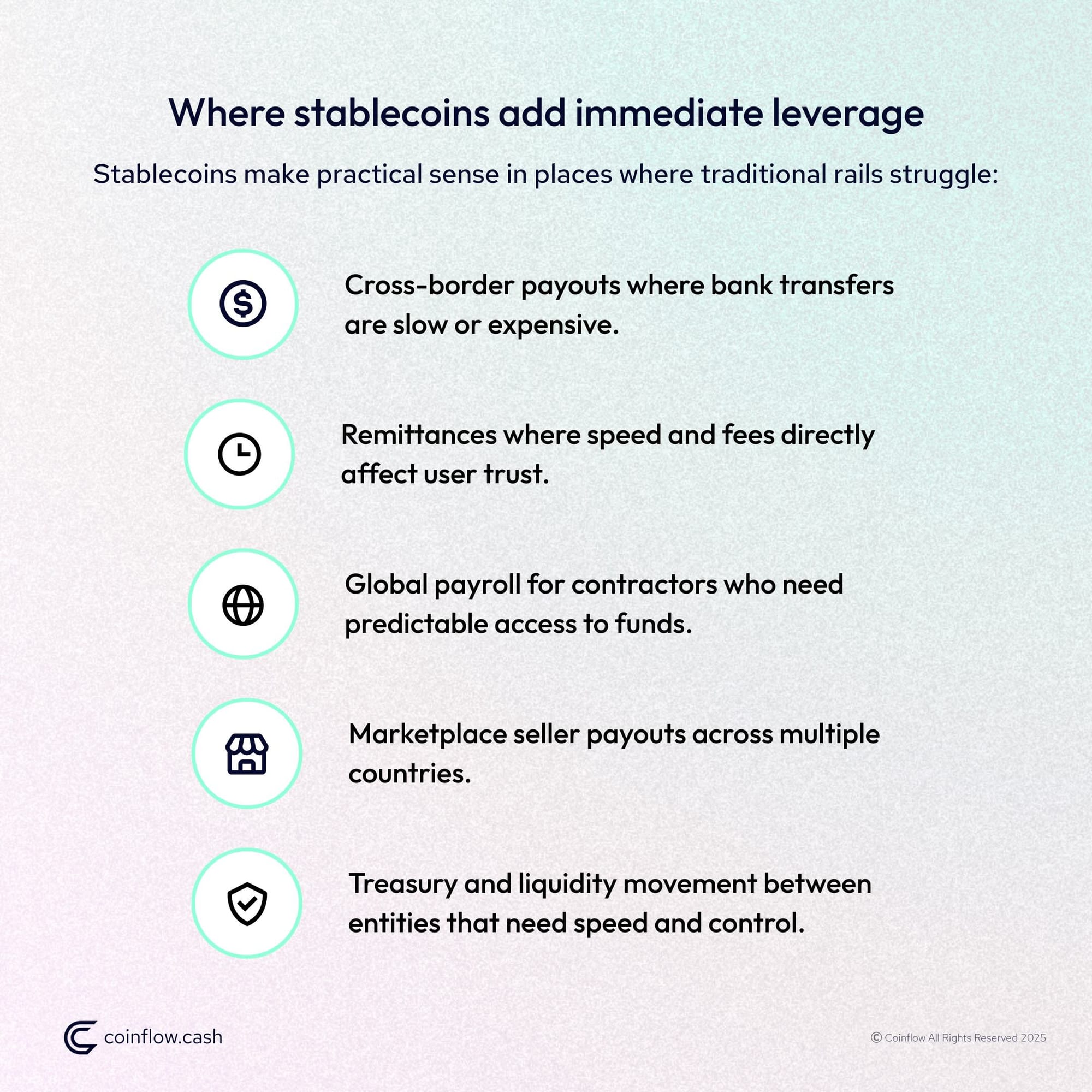

Stablecoins make practical sense in places where traditional rails struggle.

In these contexts, stablecoins reduce friction without changing the user’s mental model of “getting paid.”

They don’t eliminate the need for compliance. KYC, KYB, and monitoring still matter.

They don’t fix payout UX on their own. Users shouldn’t have to manage crypto complexity.

They don’t remove risk on the pay-in side. Fraud and disputes still exist.

The value of stablecoins depends entirely on how well they’re integrated into a broader system.

Stablecoins work best when they’re one rail inside a system that also supports traditional rails, provides settlement visibility, and reduces operational overhead. They’re a tool, not the strategy.

Before changing rails, unify how transactions are represented. Align IDs across pay-ins, fees, payouts, and settlement. Normalize statuses. Establish a clear money-movement timeline.

Remove the “two worlds” problem where revenue and disbursements live separately. Design for repeat flows like stored payment methods, subscriptions, and recurring payouts.

Reduce time-to-available-funds. Improve working capital predictability. Align settlement speed with product promises—instant where it matters, predictable where it doesn’t.

Introduce stablecoin settlement for specific corridors or use cases. Maintain a consistent operating model so new rails don’t create new blind spots.

When infrastructure aligns with how money actually moves, the effects compound.

Modernization doesn’t just make payments faster. It makes the business calmer.

Modernizing payment infrastructure isn’t about swapping tools or “upgrading tech.” It’s about redesigning how money moves so speed, security, and clarity scale together.

Coinflow is built for teams modernizing the entire money-movement lifecycle, not just checkout. By unifying tokenized pay-ins, tokenized payouts, and fast settlement visibility in one platform, Coinflow removes the fragmentation that slows teams down and creates blind spots as volume grows. Payments move through a single, coherent system (from charge to payout) without multiplying complexity.

And where stablecoins make sense, Coinflow supports them alongside traditional rails as a practical settlement option. It’s a way to move money faster across borders while keeping operations verifiable, controlled, and compliant.

The result is a payments stack that’s always-on, multi-rail, secure by design, and transparent end-to-end—so protecting users and moving fast stops being tradeoffs.

Talk to our team to see what a phased modernization plan looks like for your payment flows, and how Coinflow can simplify money movement while expanding your options, including stablecoins.

Daniel is the CEO and Co-Founder at Coinflow, connecting traditional payment rails with stablecoin technology to enable instant global settlement for trusted, cross-border commerce.

Remittance

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Remittance

Hidden FX markups, multi-day settlement, and opaque correspondent banking chains erode remittance margins. See how modern FX payment infrastructure eliminates each one.

Fintech

Real-time payments are projected to hit 22% of global transaction volume by 2028. Here's how marketplaces, e-commerce, gaming, payroll, remittance, and fintech platforms are using instant settlement to drive real business outcomes.