Remittance

Will Real-Time Payment Rails Replace Traditional Settlement?

Trapped capital, settlement delays, and batch processing are costing businesses more than they think. See why real-time payment rails are becoming the default.

Payment tokenization replaces sensitive card data with secure tokens, reducing breach risk and PCI scope while enabling safer pay-ins, payouts, and global growth.

Payment data is some of the most sensitive information your business will ever handle. Not because it’s abstractly “valuable,” but because it’s immediately usable when it leaks.

And leaks rarely come from dramatic attacks. According to Verizon’s 2024 Data Breach Investigations Report, more than two-thirds (68%) of breaches involve a non-malicious human element—everyday mistakes like misconfigured logs, third-party plugins, rushed internal tools, or data copied into the wrong environment. If card data exists anywhere in that web, your risk is real.

Payment tokenization is how modern payment stacks reduce that exposure. By keeping raw card data out of your systems, it limits breach impact, shrinks PCI scope, and enables fast, secure payment experiences as you scale.

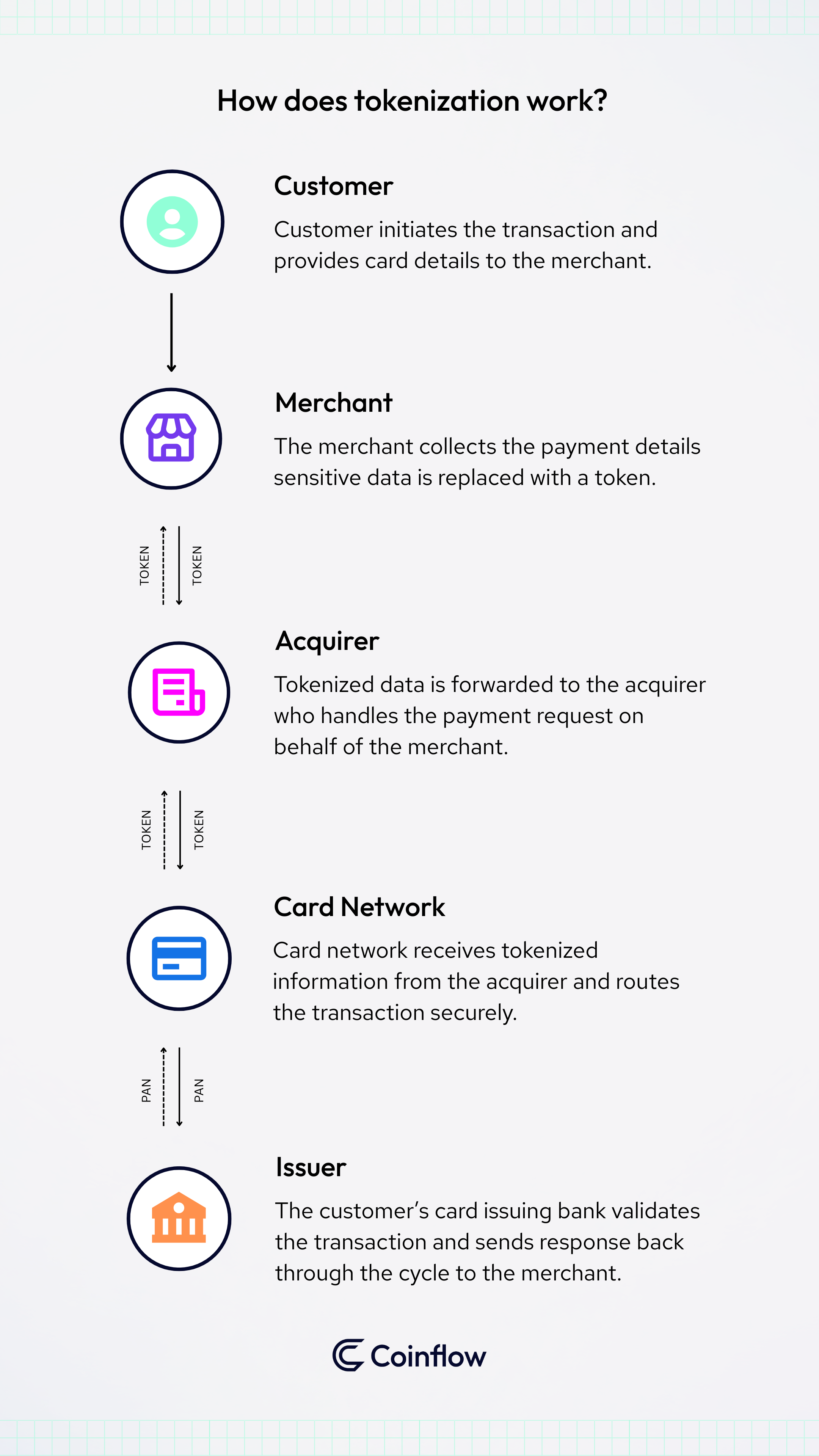

Our guide will explain how tokenization works, why it protects customer data so effectively, and how teams across ecommerce, marketplaces, gaming, fintech, and remittance use it to grow with less risk.

Payment tokenization replaces sensitive card information, like the primary account number (PAN), with a token: a random, meaningless identifier that stands in for the real card.

A token can look like a card number. It can be stored and reused. But if someone steals it, they don’t steal a usable payment credential. They steal a placeholder. Ben Meeder, Co-Founder & CTO at Coinflow, explains payment tokenization below:

The important nuance is where the real card data goes. In a tokenized setup, the PAN is stored in a secure vault that’s operated by the tokenization provider (often your PSP). Only that system can map a token back to real card data when it’s time to process a payment.

Tokenization changes how payment data moves through your product:

Tokenization often gets mixed up with two adjacent concepts:

It’s not encryption. Encryption protects data in transit or at rest by making it unreadable without a key. Tokenization removes sensitive data from your environment by replacing it with a stand-in.

It’s not masking. Masking is what users see (for example, “**** **** **** 1234”). Masking still assumes the real PAN exists somewhere in a system you control. Tokenization is about ensuring the PAN lives only in the provider vault, not in your product stack.

A customer enters their card number, expiration, and CVV at checkout (web or mobile).

Instead of your backend receiving those details, your front end uses the PSP’s JavaScript library or mobile SDK to send the sensitive data directly to the tokenization service.

The provider then does two things:

From your perspective, you never store the PAN. You store the token.

Once you have the token, you can treat it like a durable reference:

This is why tokenization is so foundational to “convenience” features that customers love: saved payment methods, subscription renewals, retries, and one-click flows.

Tokenization isn’t only for taking money. A lot of modern products also send money: to sellers, creators, drivers, players, couriers, freelancers, contractors.

Here’s the same idea applied to payouts:

A recipient enters their debit card once. The system tokenizes that payout credential. From that point on, you can pay them again and again using a token instead of storing the raw card data.

This matters a lot for platforms where payouts are frequent and operationally messy. It’s also where many “checkout-first” payment stacks fall short.

Without tokenization, card data can end up in a surprising number of places:

Internal tools built quickly to “just solve the problem”

Every place that touches PANs increases the number of things you have to secure and monitor. It also expands PCI scope.

With tokenization, your environment primarily contains tokens and non-sensitive metadata. If someone compromises your database, they don’t walk away with a list of usable card numbers.

Tokenization doesn’t magically prevent intrusion. What it does is change what an intruder can steal.

If an attacker gets into your systems and extracts tokens, they typically can’t spend them. Tokens are designed to be useless outside the system that created them.

In practical terms, tokenization can be the difference between:

PCI doesn’t disappear, but tokenization can make it far more manageable.

Because you store fewer PANs (ideally none), fewer systems fall into PCI scope. Audits tend to get simpler. Controls tend to be easier to enforce. And engineering teams spend less time chasing compliance edge cases in their own infrastructure.

A clean way to say it: tokenization shifts the hard problem (secure vaulting of card data) to providers that specialize in doing it correctly.

There’s a reason product teams love card-on-file features and risk teams fear them.

Saved cards, one-click checkout, and subscription renewals are growth levers. But they can feel like liabilities if the only way to implement them is to store sensitive data yourself.

Tokenization lets you keep the UX while dropping most of the risk. You can offer fast repeat purchases and automated renewals, without building a long-term warehouse of payment credentials inside your environment.

Tokenization and encryption solve different problems. Most modern payment flows use both.

The difference is that encryption scrambles data so it’s unreadable without keys. It’s essential for data in transit. And tokenization replaces sensitive data with a stand-in so you don’t have to store the sensitive data at all. We’ll list everything out in a table below so it’s easier to understand.

| Category | Tokenization | Encryption |

|---|---|---|

| What it does | Replaces sensitive data (e.g., PAN) with a random, meaningless token | Scrambles sensitive data so only someone with the right key can read it |

| Reversibility | Irreversible without access to the secure vault | Reversible using encryption keys |

| Ideal use cases | Long-term storage: card-on-file, recurring billing, payouts | Data in transit: checkout submission, API communication |

| Where sensitive data lives | Only inside the PSP’s PCI vault | In encrypted form, wherever it’s stored or transmitted |

| Impact on PCI scope | Significantly reduces merchant PCI scope | Does not remove PCI scope; encrypted data is still considered sensitive |

| Security strength | Tokens have no exploitable value if stolen | Encryption strength depends on key management and the algorithm |

| Operational considerations | Requires token lifecycle management (create/store/reuse/delete) by provider | Requires key rotation, key storage, and encryption policies |

| Risk if breached | Attackers get useless tokens, not card numbers | Attackers may decrypt if keys are compromised |

| How they work together | Protects data at rest and in reuse | Protects data in transit |

In a typical flow:

That combination is what keeps you from ending up with “encrypted PANs” sitting in your own database forever, which can still create significant risk if keys or systems are compromised.

Tokenization powers the payments that drive retention:

If a plugin, extension, or admin tool gets compromised, tokenization helps ensure the attacker doesn’t get a dump of usable card numbers. It also keeps PCI from ballooning as you expand to more markets.

Marketplaces have a two-sided security problem: buyers and sellers.

Tokenization helps you store buyer payment methods without storing PANs, and it can also tokenize payout credentials so you’re not keeping seller or creator card data inside your operations stack.

That matters because the operational surface area of a marketplace is huge: internal tooling, payouts workflows, support systems, and reconciliation pipelines. Tokenization reduces the odds that any one of those becomes a high-impact breach vector.

Gaming is often high fraud, high velocity, and high emotional stakes for users.

Tokenization protects:

The business benefit is not just “safer.” It’s also calmer operations: fewer fire drills when fraud spikes, fewer catastrophic scenarios where compromised systems leak payment credentials.

These products can store payment methods for both senders and recipients. They also operate across jurisdictions where the compliance burden compounds quickly.

Tokenization helps reduce exposure across regions, simplifies the compliance story, and supports recurring transfers and frequent payouts without turning your database into a repository of sensitive card data.

Payment tokenization is one of the rare infrastructure decisions that improves both security and product performance at the same time.

It keeps sensitive card data out of your systems, reduces the impact of breaches, and shrinks your PCI burden. Just as importantly, it enables the fast, modern payment experiences customers now expect, including saved cards, subscriptions, and instant payouts.

But tokenization alone isn’t the differentiator anymore. The real difference is whether it stops at checkout, or extends across the full movement of money your product depends on.

Coinflow is built around tokenized pay-ins and tokenized payouts, allowing teams to support card-on-file and recurring payment experiences while also sending funds to users securely, without warehousing sensitive payout credentials inside their own systems. As products scale globally, that foundation becomes even more critical.

By pairing tokenization with fast settlement options, built-in risk tooling, and support for modern rails and international payment flows, Coinflow turns data protection from a defensive measure into a foundation for safer growth. The result is a payments stack that doesn’t slow teams down, but instead enables faster launches, simpler compliance, and more resilient operations as volume and complexity increase.

If you want to protect customer data and move faster, Coinflow helps you build tokenized payment flows that scale globally without ballooning risk.

Talk to our team to see how tokenization and instant settlement can accelerate your roadmap while keeping customer data protected.

Nothing useful to the attacker. A token has no mathematical relationship to the original card number: it can't be reversed, decoded, or used outside the specific system it was created for. As the article puts it, a stolen token is worthless. This is the core difference from encryption, where a compromised key could theoretically unlock the original data.

Yes. Advanced tokenization solutions cover both sides of the money flow. Customer cards are tokenized at checkout for pay-ins, and recipient debit cards are tokenized for outbound payouts. This means your platform never stores raw card numbers for buyers or sellers, securing the full payment lifecycle.

Not exactly, but it dramatically reduces the burden. PCI compliance still applies to whoever handles the raw card data (your payment provider). What tokenization does is shrink your PCI scope by ensuring raw PANs never touch your systems. Fewer systems handling sensitive data means fewer systems to audit, which translates to lower compliance costs and less operational risk for your team.

Customers typically don't notice tokenization at all, and that's the point. Behind the scenes, it enables features like saved cards, one-click checkout, and subscription renewals without requiring your systems to store sensitive payment data. The experience gets smoother, not more complicated.

John Thomas Lang is Head of Marketing at Coinflow and a two-time $1B-unicorn brand builder known for turning early-stage companies into high-growth, category-defining businesses.

Remittance

Trapped capital, settlement delays, and batch processing are costing businesses more than they think. See why real-time payment rails are becoming the default.

Remittance

Faster settlement, lower costs, freed working capital. See how crypto payment rails actually move money today, and why fintechs are switching from legacy infrastructure.

Remittance

Stop losing gig workers to slow payments and hidden FX fees. Learn why legacy rails like ACH and Wires fail global platforms and how a single API integration can unlock instant, compliant payouts across 40+ countries with zero fraud liability.