SaaS

PayFac as a Service: The Buyer’s Guide for SaaS Platforms

Most SaaS platforms leave $150K+ on the table every year. PayFac as a Service fixes that if you pick the right category.

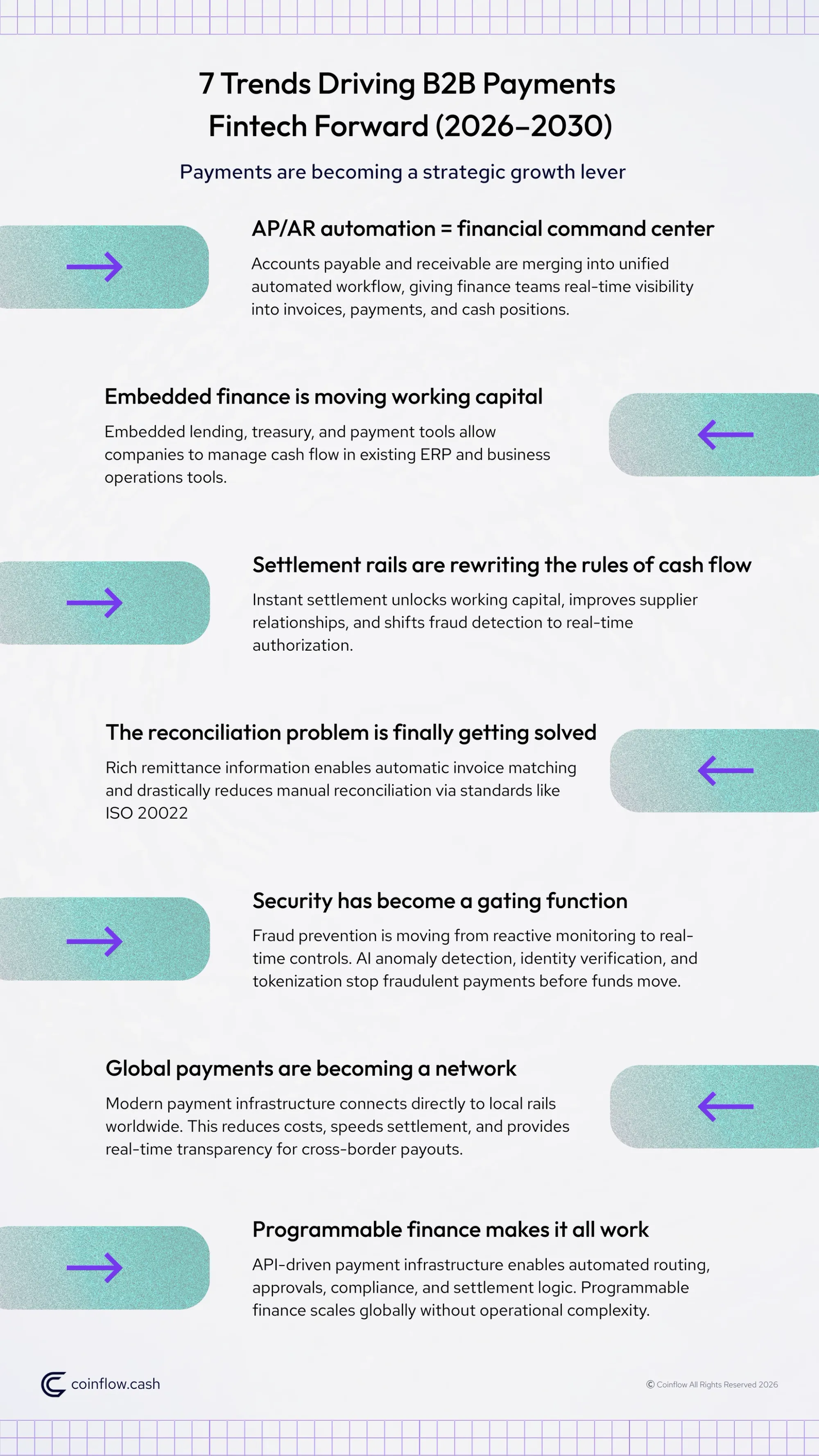

B2B payments fintech is reshaping how businesses move money in 2026 and beyond, spanning AP/AR automation, embedded finance, instant settlement, and AI-driven fraud prevention. Here’s what finance leaders need to know.

For decades, B2B payments operated like plumbing: invisible when they worked, catastrophic when they didn't. Checks cleared in days. Reconciliation lived in spreadsheets. And "payment strategy" meant choosing between wire transfers and ACH. That era is over.

The global B2B payments market is projected to reach $1.67 trillion this year and surpass $3.4 trillion by 2031, while the embedded B2B finance market has already hit $4.1 trillion and is expected to quadruple by 2030. CFOs and finance teams are driving that growth because they've stopped treating payments as a cost center and started treating them as a growth lever. The platforms winning today settle faster, reconcile automatically, and embed financial intelligence directly into operational workflows.

Here's how that's playing out across seven critical areas.

Accounts payable and accounts receivable used to be separate back-office functions, each running their own workflows, tools, and timelines. AP/AR automation is collapsing those silos into a single operational layer that handles invoice capture, approval routing, payment execution, remittance delivery, and reconciliation in a continuous flow.

The real value goes beyond efficiency. Unified AP/AR rethinks the cash conversion cycle entirely. When AP and AR operate as a single system, finance teams gain real-time visibility into what's owed, what's been paid, and where cash is at any given moment. That visibility feeds directly into treasury management, working capital planning, and supplier relationship strategy.

The latest evolution is task-specific AI agents that handle exception management, the work that used to eat up the last week of every month. These agents catch duplicate invoices before they're paid, flag unusual payment patterns in real time, and automate accrual calculations that previously required manual spreadsheet work.

The result: fewer surprises at month-end close, and finance teams that spend their time on analysis rather than data entry.

For payout-heavy platforms, however, AP/AR automation alone only addresses half the equation. The other half, actually executing payments, orchestrating payouts across multiple parties, and ensuring everything reconciles, requires purpose-built payment infrastructure that connects directly into your operational stack.

Embedded finance has been around for years. Ride-sharing apps embedded payments long ago. E-commerce platforms added buy-now-pay-later buttons. But in 2026, embedded finance is hitting B2B with a force that dwarfs consumer use cases, because the transaction volumes and working capital flows involved are orders of magnitude larger.

The concept is straightforward: instead of forcing finance teams to toggle between payment platforms, banking dashboards, and treasury tools, embedded finance brings lending, risk controls, and treasury functions directly into the ERP or platform where operational data already lives. Research from Galileo (previously cited) shows that 63% of U.S. B2B service providers now offer some form of embedded finance solution to business clients.

For CFOs, the appeal is practical. Embedded finance improves cash predictability without adding new systems or vendor relationships. Working capital decisions happen alongside the supplier data, invoice history, and payment schedules that inform them, rather than in a separate dashboard three tabs away.

Tighter liquidity conditions in 2026 are accelerating demand. When capital is harder to access, the ability to earn yield on idle balances, activate treasury functions without moving funds off-platform, and free trapped working capital through instant settlement becomes a genuine competitive advantage.

Traditional payment rails were designed for a batch-processing world. Payments went out in groups, settled over days, and arrived with minimal information attached. That model is breaking under the weight of real-time commerce.

The shift toward instant settlement is now backed by infrastructure at the national level. The FedNow Service surpassed 1,500 participating financial institutions by late 2025, a 44% increase from the year prior, and now spans all 50 states. Europe's SEPA Instant scheme handled 14.5 billion transactions in 2024, up 54% year-over-year.

The direction is clear: real-time is becoming the baseline expectation.

Speed matters, but the downstream effects matter more. When settlement compresses from days to seconds, three things shift simultaneously:

| Legacy Workflows | Modern Fintech Workflows | |

|---|---|---|

| Settlement timing | 2–5 business days | Seconds |

| Reconciliation | Manual matching | Automated with structured data |

| Working capital access | Off-platform treasury tools | Embedded in operational architecture |

| Security model | Reactive, post-breach | Gating function at authorization |

Even leading processors like Stripe still operate on multi-day batch settlement for standard payouts. Platforms that need instant settlement and real-time payout orchestration are finding that the legacy incumbents weren't built for this speed.

Stripe settles in days. Coinflow settles in seconds. For payout-heavy platforms where settlement speed directly impacts seller retention and working capital, that gap changes the operating model. See how the two stack up.

Ask any finance team what keeps them up at night, and reconciliation will be near the top of the list. Money moves just fine. The challenge is that when it arrives, no one can match it.

Payment confirmations show up without invoice numbers. Reference fields get truncated by intermediary banks. Remittance data sits in email attachments instead of traveling with the payment.

The result: finance teams spend hours every week matching bank statements against invoices, chasing missing details, and resolving discrepancies manually.

The global adoption of ISO 20022, a structured messaging standard for payments, is changing this. The Fedwire Funds Service completed its migration to ISO 20022 in July 2025, and adoption is accelerating across global corridors.

ISO 20022 enriches payment messages with invoice details, FX rates, and remittance data in designated fields. When payment messages carry this structured data, reconciliation can happen automatically. Software can match payments against open invoices without human intervention. Exceptions surface in real time instead of festering until month-end.

The implication for B2B platforms is significant: suppliers that send clean, structured remittance data will get paid faster and face fewer disputes. Data completeness is becoming the new early-payment discount.

For fintech platforms and marketplaces managing multi-party flows, eliminating the reconciliation black hole means turning payment data into a strategic asset, one that informs decisions, reduces operational overhead, and builds trust with every transaction.

If there's one statistic that captures the urgency of payment security in 2026, it's this: business email compromise attacks surged 1,760% between 2022 and 2023 following the popularization of generative AI tools. BEC went from representing just 1% of all cyberattacks in 2022 to 18.6% in 2023.

The FBI's Internet Crime Complaint Center reported that BEC cost global organizations nearly $55.5 billion over the decade ending in December 2023. And 70% of organizations were targeted by attempted BEC attacks in the last year alone, according to Arctic Wolf's 2024 Trends Report.

Every one of these threats hits finance teams directly, through invoice fraud, account takeover, synthetic identities, and social engineering attacks that exploit the inherent trust in business relationships.

The shift in 2026 is moving security from a reactive, post-breach function to a gating mechanism that operates at authorization. Three layers are converging:

For platforms scaling transaction volume, security needs to be embedded into the payment flow itself, operating invisibly at checkout and authorization while protecting revenue and reputation.

Coinflow pairs AI-driven fraud prevention with 100% chargeback indemnification and built-in AML/KYC compliance, so platforms can grow transaction volume without expanding their sensitive-data footprint or taking on dispute liability.

Talk to our teamCross-border B2B payments have historically been expensive, slow, and opaque. Funds bounce through correspondent banks, each adding fees, delays, and uncertainty. Suppliers in one country wait days to learn whether a payment from another country actually arrived.

Modern B2B payments fintech treats global payments like a network. Single integrations connect to local rails in multiple markets, bypassing correspondent banking chains entirely. Multi-currency FX happens at transparent rates. Settlement tracking provides real-time visibility so suppliers know exactly when funds will arrive.

The cross-border payments segment is projected to hold a dominant 59.6% share of the overall B2B payments market in 2026, driven by expanding global trade and the increasing number of cross-border transactions involving multiple buyers, suppliers, and intermediaries.

For remittance platforms, payroll providers, and marketplaces managing international seller payouts, payment reliability directly impacts trust, retention, and the ability to expand into new corridors. When suppliers and sellers know exactly what they'll receive and when, disputes drop and relationships strengthen.

Underneath all of these shifts (automation, embedded finance, real-time settlement, security) sits a layer of API-driven infrastructure that makes them possible.

Programmable finance means payment logic can be customized without code changes or vendor support tickets. Teams define rules for fund release, rail routing, and approval thresholds. Amount, recipient, and payment type trigger the right workflow automatically. These rules adapt to changing business conditions without requiring engineering resources every time a new corridor, currency, or compliance requirement enters the picture.

Integration with existing ERP platforms, accounting software, and treasury tools happens through standard APIs rather than custom connectors that break with every software update. For B2B payments fintech, this means platforms can scale without accumulating technical debt. New payment methods, currencies, or regulatory requirements plug into existing infrastructure instead of requiring parallel systems.

The next frontier is autonomous, agent-initiated actions across commerce and payments: systems that don't just execute pre-defined rules but make contextual decisions about routing, timing, and risk based on real-time data.

Every trend in this article points in the same direction: payments infrastructure needs to be faster, smarter, and more deeply integrated into the platforms that depend on it.

Coinflow is purpose-built for that reality. A single API handles pay-ins, payouts, FX orchestration, and reconciliation across 100+ markets with instant settlement, so working capital stops sitting idle in batch queues.

Tokenized checkout and built-in AML/KYC keep platforms compliant at scale without expanding PCI scope. And 100% chargeback indemnification means dispute costs are predictable and liability stays off your books.

For marketplaces, fintech platforms, and cross-border operations where settlement speed shapes unit economics, talk to our team about what that infrastructure looks like in practice.

Sources linked throughout. All market data referenced from publicly available research reports and government publications as of March 2026.

Daniel is the CEO and Co-Founder at Coinflow, connecting traditional payment rails with stablecoin technology to enable instant global settlement for trusted, cross-border commerce.

SaaS

Most SaaS platforms leave $150K+ on the table every year. PayFac as a Service fixes that if you pick the right category.

SaaS

There's no single best embedded payments provider — there's the right category for your platform's GPV, geography, and business model. Here's how to find yours in under 10 minutes.

Fintech

Real-time payments are projected to hit 22% of global transaction volume by 2028. Here's how marketplaces, e-commerce, gaming, payroll, remittance, and fintech platforms are using instant settlement to drive real business outcomes.