Risk & Compliance

How to Build an AML Policy That Actually Holds Up Under Scrutiny

Your AML policy is what you say you do. Your program is what you actually do, and only the program holds up under regulator and bank-partner scrutiny.

Transaction monitoring catches structuring, layering, and mule activity, but the real exposure is the gap between alert and action. Here's what matters.

Every compliance team knows when an alert is fired. The question that determines your exposure is what happened immediately after it did.

Modern rule engines evaluate each transaction in real time while aggregating behavioral patterns. Structuring, layering, and velocity drift over days to weeks before surfacing typologies that no single transaction reveals. The expensive part is the window between an alert firing and an analyst dispositioning it, because the flagged actor keeps transacting the entire time.

That's where dollar exposure compounds and where examiner findings originate. U.S. merchants now spend $4.61 for every $1 lost to fraud, a 32% increase since 2022 per the 2025 LexisNexis True Cost of Fraud Study, and the bulk of that multiplier is investigation labor and remediation, not the face value of the transaction.

This piece covers what transaction monitoring catches after onboarding, the typologies it's built to recognize, and why response speed matters more than detection sophistication.

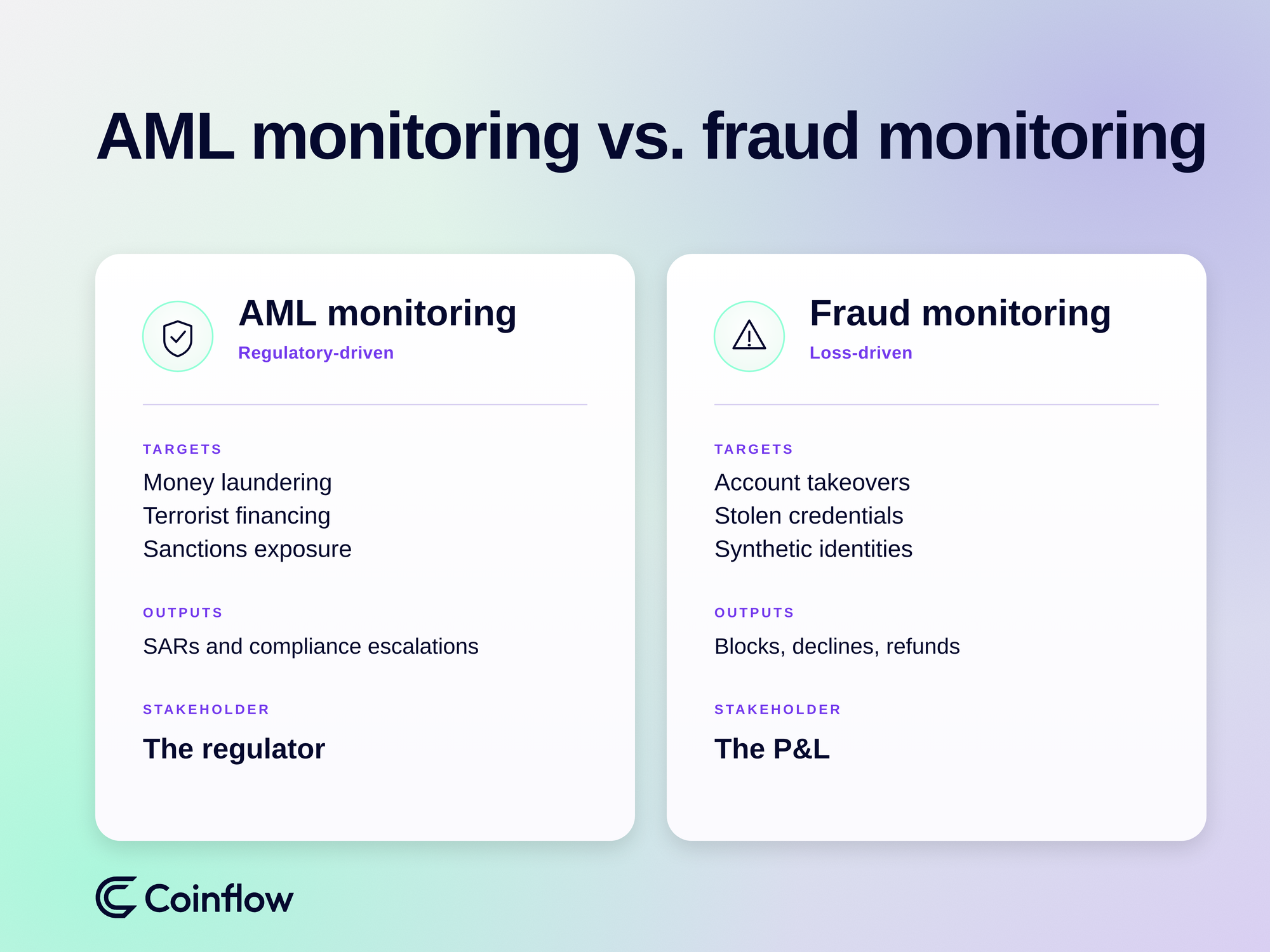

The two terms get used interchangeably. They share data pipelines and often run on the same infrastructure, but they answer to different stakeholders.

It targets money laundering, terrorist financing, and sanctions exposure, and its outputs are Suspicious Activity Reports (SARs) and escalations to a compliance officer. The stakeholder is the regulator.

It targets unauthorized transactions, account takeovers, stolen credentials, and synthetic identities. Its outputs are blocks, declines, and refunds. The stakeholder is the P&L. The two can overlap on a single actor, but more often they're distinct problems requiring distinct dispositions. A third category, chargebacks, runs on the same detection layer and gets covered below.

Transaction monitoring evaluates live behavior against an established baseline. When a platform onboards a merchant, it sets that baseline by establishing identity: what the merchant uses the platform to sell, and what normal activity looks like. From there, the system monitors deviations from known laundering and fraud typologies.

Amounts deliberately engineered to stay below reporting thresholds. In the U.S., many transaction types trigger a Currency Transaction Report above $10,000, so a steady cadence of $9,999 transactions is a classic structuring flag. Each transaction looks routine on its own; the aggregate is the signal.

Funds are split and move across accounts or currencies to obscure their origin. A user receives a transfer, fragments it across wallets, converts a portion, and then consolidates it into a single withdrawal. Velocity and fragmentation are the tells.

Legitimate accounts weaponized to move funds for a third party. The account holder's profile — age, geography, transaction history — doesn't match the sudden inflows and rapid outflows. Catching this requires behavioral baseline comparison, not threshold triggers alone.

Flows into or out of monitored regions. As of the February 2026 plenary, the Financial Action Task Force lists 22 jurisdictions under increased monitoring, and even small transfers tied to those regions warrant enhanced scrutiny.

On the fraud side, the common tell is testing: an actor with a stolen card runs a few small transactions to confirm it works, then escalates fast, sometimes to six figures in a single day. More broadly, a customer's profile drifts — volume doubles, new counterparties appear, timing shifts — and multiple simultaneous changes trigger escalation. A single change is usually explainable. Several at once rarely are.

The point isn't to flag every anomaly. It's to recognize the patterns that indicate structured financial crime and surface them while there's still time to act.

An alert stops nothing on its own. When a rule fires, the laundering, fraud, or chargeback activity is still in motion. The alert is the first step, not the resolution, and every monitoring program moves through the same five stages.

Every hour between alert and disposition is another hour the actor keeps moving funds. Dollar exposure grows linearly.

The U.S. Financial Crimes Enforcement Network (FinCEN) requires SAR filing within 30 days of detecting a suspicious transaction, with a 60-day extension available when no suspect is identified (31 CFR 1020.320).

The clock starts at detection, not disposition which is exactly why time in queue is a regulatory exposure, not just an operational one.

Take a layering typology generating hundreds of modest-value alerts. Missing detection on a single $5,000 transaction costs $5,000. Missing the same actor's behavior for 72 hours while the alert sits in the queue can cost $500,000 or more because the actor keeps moving funds through the platform uninterrupted.

Speed compresses every component of that cost. Faster triage cuts analyst hours per case. Faster disposition limits the actor's transaction window. Faster SAR filing satisfies regulatory timelines. A platform that resolves an alert in two hours instead of 48 doesn't just save labor; it cuts the amount the actor moves by roughly 96%. That's the case for treating response time, not detection coverage, as the metric that actually governs exposure.

Detection quality is table stakes. What separates a resilient monitoring layer from a compliance checkbox is the operational infrastructure around it. The checklist for evaluating a payments partner:

There's also a scale advantage a single operator can't replicate. A merchant watching its own dashboard sees only its own volume and customers. A payments platform serving many merchants sees patterns across the entire industry, enabling it to build vertical-specific rules and construct a single identity for each cardholder across the portfolio.

That enables cross-merchant rules and, in some cases, merchant-specific rules informed by activity seen elsewhere — the kind of backstop that catches a problem at $5,000, well before it reaches $500,000.

If response speed is the variable that governs exposure, then the constraint isn't how good your analysts are. It's whether the infrastructure underneath them surfaces alerts fast enough to act on, with enough context to disposition without a second investigation.

That's a build-versus-buy question most compliance functions answer the hard way. Real-time evaluation on every transaction, tunable typology rules by vertical, risk-scored queues, sanctions screening on the same pipeline, and an audit trail clean enough to survive an exam — assembling that in-house is a multi-quarter engineering effort that competes with the roadmap. The alternative is a payments layer that ships it by default.

This is where a platform serving many merchants pulls ahead of any single operator. Coinflow evaluates every transaction across its portfolio in real time, so the rules aren't limited to a single merchant's history. Cross-merchant identity, vertical-specific patterns, and drift detection flag unusual behavior while the actor is still on the platform, and every alert produces audit-ready records by default. (Novig runs its sports trading platform on exactly this backstop.) The result is a compliance team that dispositions alerts in hours, not days.

Detection was never the hard part. The platform that closes the gap between alert and action is the one that actually controls its exposure. See how Coinflow builds transaction monitoring into its payments infrastructure.

Karan Sethi is Risk & Compliance Manager at Coinflow. Karan has nearly a decade of fintech experience from his time at PayPal and J.P. Morgan. He holds a degree in Finance from Purdue University.