SaaS

5 Best Alternatives to Stripe Connect for Embedded Payments

Most platforms outgrow Stripe Connect the moment payments get serious. Here are five alternatives for embedding payments, from interchange-plus to full PayFac.

ISVs now handle payments for 90% of U.S. small businesses. See how software became the payments channel, and what it means for platforms still on the sidelines.

Walk into any small business today — a fitness studio, a dental practice, a neighborhood restaurant — and ask the owner who handles their payments. You won't hear the name of a payment processor. You'll hear the name of their software.

Software companies that run the day-to-day operations of small and mid-sized businesses have quietly become the front door to payments. The merchant doesn't think about who's settling the funds or routing the card data. They think about the platform they log into every morning, and whoever owns that login owns the relationship.

For independent software vendors (ISVs), this has rewritten the rules of what a software business can be. Payments are no longer a feature a platform passes through to a third party. They're the second product. And in many cases, they're becoming the bigger one.

The traditional payments stack treated software and processing as two separate purchases. A merchant signed up with a processor, integrated their software, and reconciled the two systems by hand. Anyone who has run a small business knows what that looked like in practice: exporting CSVs at the end of the day, chasing mismatched line items, calling two different support lines when something broke.

ISVs collapsed that model. By embedding payments directly inside the software a merchant already uses, transactions started living in the same place as bookings, invoices, and inventory. The integration happens through APIs and SDKs that let a software developer plug card acceptance, ACH, payouts, and reporting into their product as native functionality. To the merchant, payments stop being a separate product. They become a feature of the thing they already trust.

That convenience compounds. A salon platform that charges a card the moment a booking is confirmed has eliminated an entire category of administrative work. A dental practice management suite that reconciles every payment to the invoice it came from has eliminated a job function. Once a merchant experiences that, going back to a standalone processor feels like going back to paper.

The user-experience case for embedded payments has been clear for years. What's changed more recently is the financial case for the software companies themselves.

Andreessen Horowitz's analysis of vertical SaaS found that adding embedded fintech can lift revenue per customer by 2x to 5x. A platform charging $200 a month for software can plausibly capture $1,000 a month per customer once payments are layered in. That isn't an upsell — it's a different business altogether.

The proof is sitting in public earnings reports. Toast's payments revenue now makes up the majority of its top line. Shopify Payments handles the bulk of GMV on the platform. ServiceTitan processes tens of billions of dollars in transaction volume across its contractor base.

None of these companies started as payment processors. They became processors because their customers were already running their businesses on the software, and the payments revenue was sitting there waiting to be captured.

McKinsey's 2026 research on ISV maturity puts numbers behind the trend at the channel level.

The ISV channel, by McKinsey's measure, is now growing roughly three times as fast as traditional payments distribution.

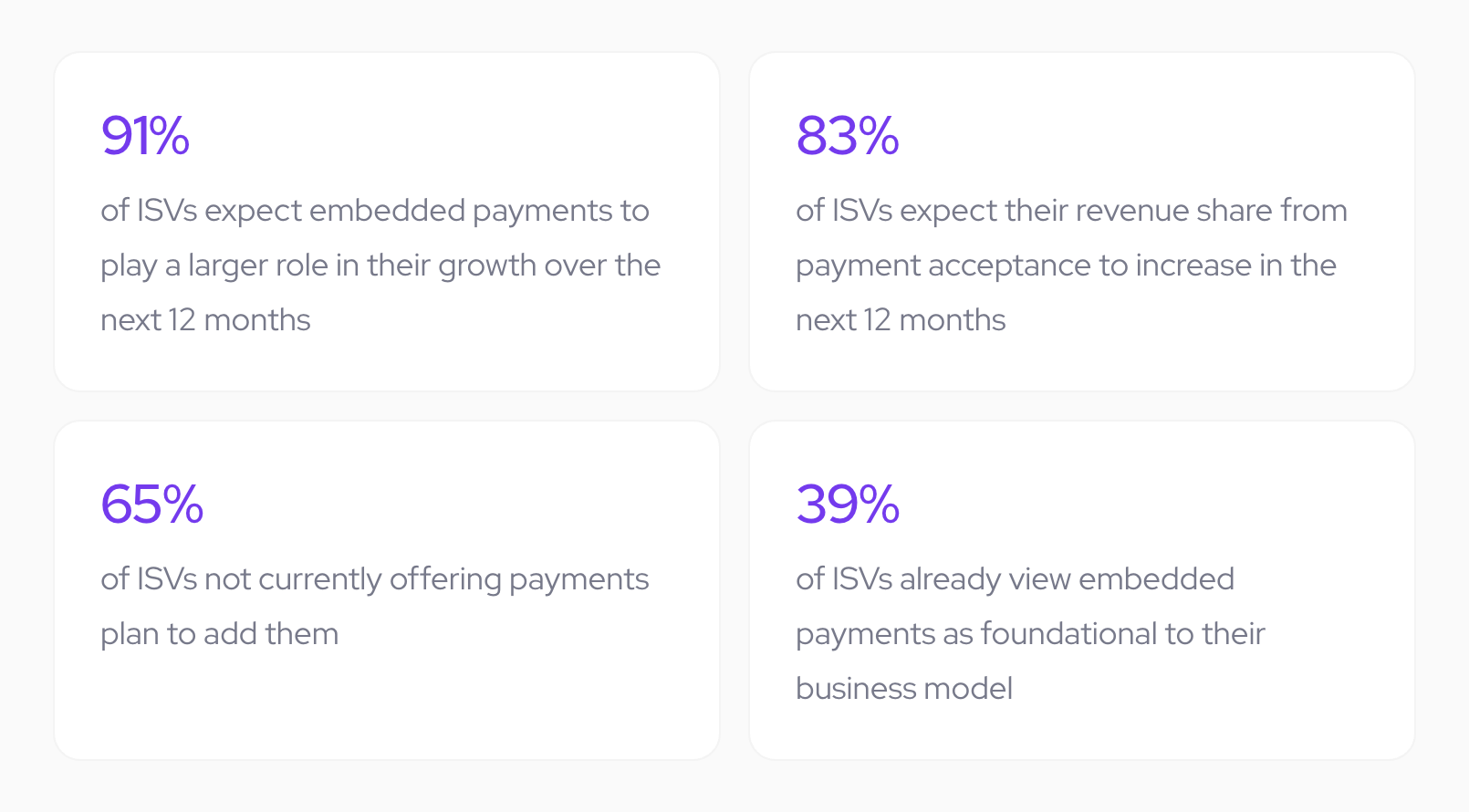

The mood inside the ISV market matches the data. An August 2025 Stax survey of 300 U.S.-based payment professionals across ISVs found that 91% expect embedded payments to play a larger role in their growth strategy over the next 12 months — with more than half saying that role will be much larger.

What that survey describes isn't a market deciding whether embedded payments are worth pursuing. It's a market that's already decided, and is now racing to execute.

The ambition is one thing. The execution is harder, and most early-stage ISVs hit the same wall in roughly the same way.

The default starting point is Stripe Connect, because it's the easiest thing to integrate. The problem isn't the integration, it's what happens after launch. The platform ends up shouldering the payments relationship — onboarding questions, payout disputes, chargeback investigations — without capturing the revenue that comes with it.

The deeper issue is structural. Flat-rate, off-the-shelf platforms are built to acquire merchants efficiently, not to make ISVs profitable. Once a software company has product-market fit, the binding constraint shifts from customers to payments economics.

That's also when the question of which payment model an ISV actually operates under starts to matter, because the gap between flat-rate ISV economics and a real revenue share isn't a matter of pricing tweaks. It's a matter of infrastructure. The gap between a default setup and infrastructure built for ISV economics looks like this:

| Stripe Connect | Coinflow Launchpad | |

|---|---|---|

| Pricing model | Flat-rate (2.9% + $0.30) | Interchange-plus from day one |

| ISV revenue share | Minimal to none | Real share on every transaction, improves with volume |

| Submerchant settlement | 2 business days | Instant, at time of transaction |

| Onboarding | Days, often manual follow-up | Minutes, automated KYC and underwriting |

| Payment splits | Manual reconciliation | Automatic, at the moment of transaction |

| Chargeback liability | ISV/submerchant carries risk | Indemnified |

| Support | Help center | Named engineer, 24/7 |

Moving to interchange-plus pricing, capturing a real revenue share, and offering instant settlement to submerchants are the differences between payments as a pass-through cost and payments as a meaningful revenue line.

A handful of criteria separate payments infrastructure built for software platforms from infrastructure that merely tolerates them:

The ISVs that win long-term are the ones that treat payments as a product, not a feature. The infrastructure underneath has to be designed for that.

Coinflow Launchpad was built to close exactly this gap. It's an accelerator program for early-stage ISVs — typically under $10M ARR, with 20 to 1,000 submerchants — that want the economics and infrastructure of an enterprise payments partnership without having to wait until they qualify for an enterprise contract.

Launchpad members get interchange-plus pricing from day one, revenue share on every submerchant transaction, automatic payment splitting, instant settlement for their submerchants, automated KYC and underwriting, and 24/7 integration support from a named Coinflow engineer, across more than 100 ISV verticals.

There are two tracks: a side-by-side migration path for ISVs already on Stripe Connect, and a from-scratch path for new builders who want the infrastructure right the first time.

The platforms that embed payments now will own the full customer relationship for the next decade. The ones that wait will be competing against platforms that already do. If you're building an ISV and want to see what the economics could look like for your platform, apply to Launchpad or get in touch with our team.

Daniel is the CEO and Co-Founder at Coinflow, connecting traditional payment rails with stablecoin technology to enable instant global settlement for trusted, cross-border commerce.

SaaS

Most platforms outgrow Stripe Connect the moment payments get serious. Here are five alternatives for embedding payments, from interchange-plus to full PayFac.

SaaS

Most SaaS platforms leave $150K+ on the table every year. PayFac as a Service fixes that if you pick the right category.

SaaS

There's no single best embedded payments provider — there's the right category for your platform's GPV, geography, and business model. Here's how to find yours in under 10 minutes.