Remittance

5 Best Payment Gateway Services Built for Global Growth

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Where do blockchain cross-border payments actually fit in your stack? A guide for the platforms, fintechs, and marketplaces moving money across borders.

Moving money across borders is still one of the slowest, least predictable parts of running a global platform. A buyer in São Paulo pays on a Tuesday. The seller in Manila sees the funds Friday, if the timing lines up. Multiple correspondent banks touch the transaction, each adding a fee, a delay, and another reconciliation headache.

Blockchain cross-border payments are reshaping that experience, not by replacing the financial system but by sitting underneath it as a faster settlement layer.

For the software platforms, fintechs, marketplaces, and remittance providers building the next generation of global products, the question is no longer whether blockchain has a role in cross-border money movement. The question is where exactly it fits, and how to integrate it without forcing end users to touch crypto.

The global cross-border payments market is on track to reach $397 billion in 2026 and $727 billion by 2034, driven by digital commerce, remittances, and global SaaS. But the underlying infrastructure has not kept pace. The World Bank reports that sending $200 internationally still costs an average of more than 6%, well above the United Nations Sustainable Development Goal target of 3%.

Three structural issues create that friction:

Blockchain rails address all three. Settlement is direct, continuous, and final.

In practice, the cross-border use case has converged almost entirely on stablecoins, not on volatile cryptocurrencies. Stablecoins are dollar-pegged tokens (most commonly USDC and USDT) that move on public blockchain networks like Solana, Ethereum, and Base.

The mechanic is what matters. A platform receives funds in local currency, converts to a stablecoin, moves it across borders in seconds, and converts back to the recipient's local currency. The stablecoin exists only during settlement. Often called the "stablecoin sandwich," this approach gives platforms blockchain speed without asking customers to hold digital assets.

The numbers say this is no longer fringe infrastructure. According to Visa's onchain analytics, adjusted stablecoin transaction volume reached roughly $28 trillion in 2025, with real-world payments volume doubling to about $400 billion, 60% of which is estimated to be B2B. Bessemer Venture Partners reports that fiat-backed stablecoin supply exceeded $273 billion in March 2026, up roughly 40x from $6.8 billion in March 2020.

For platforms evaluating where to apply blockchain rails, the answer is rarely "everywhere." It's "specific corridors where traditional rails fail." A domestic ACH transfer doesn't need stablecoin settlement. A payout to a contractor in the Philippines or a remittance to Mexico does.

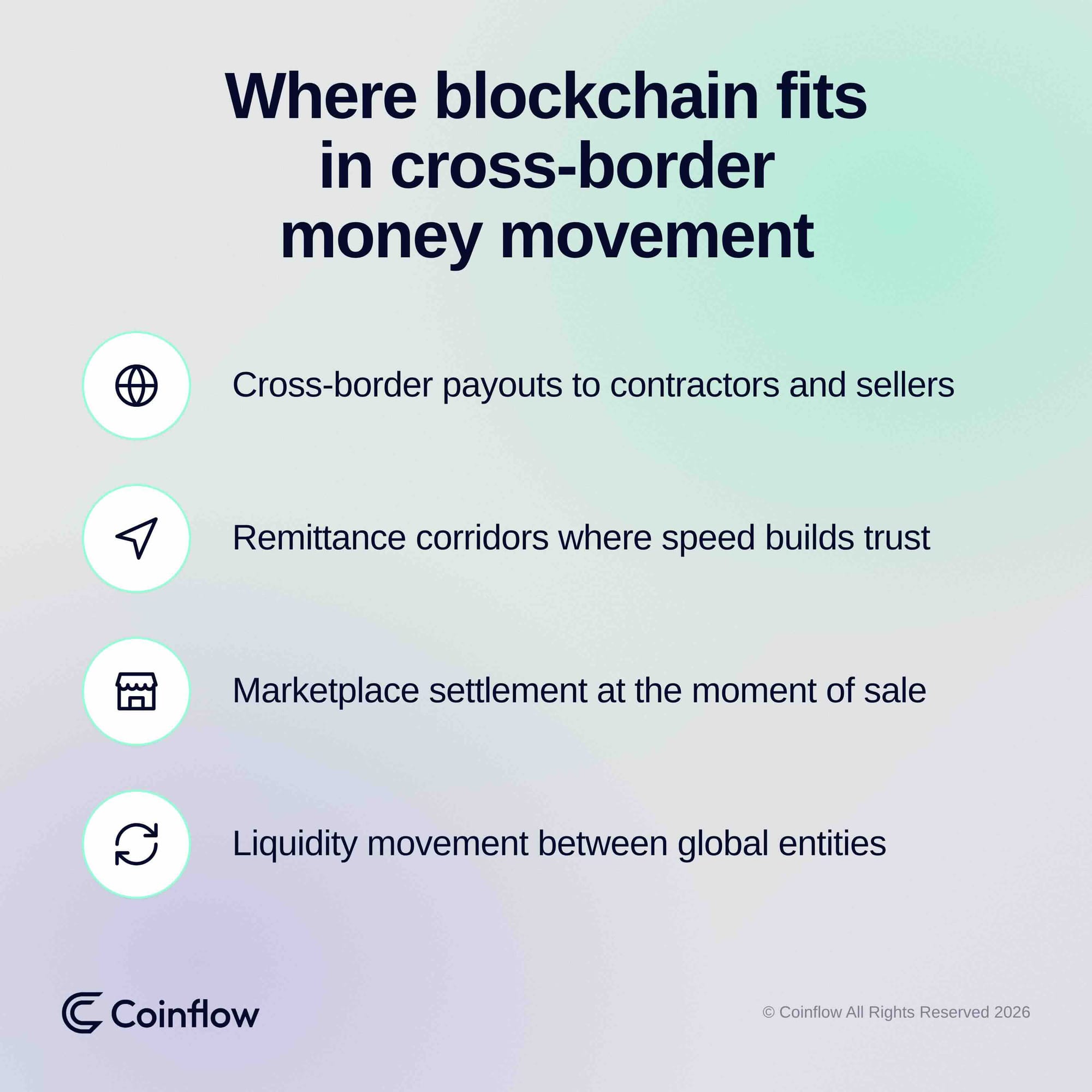

The clearest fits:

Blockchain does not fix every cross-border problem on its own. KYC, KYB, and transaction monitoring still apply. Fraud and chargebacks on the pay-in side still need to be managed. And the last-mile problem, converting stablecoins back to local currency through trusted off-ramps, requires real banking relationships and FX orchestration underneath.

Remittance platforms compete on speed, cost, and reliability in markets where traditional banking access is limited. Pre-funding accounts across multiple LATAM, African, or Southeast Asian destinations ties up working capital that could otherwise fund growth.

Félix, a WhatsApp-based remittance platform sending money from the U.S. into Latin America, used Coinflow's instant stablecoin settlement to eliminate that capital drag. Faster settlement, lower costs passed to end users, and easier expansion into new corridors followed.

Fintechs serving freelancers, contractors, and gig workers face a recurring problem: getting USD-denominated earnings into local accounts quickly, reliably, and without losing margin to FX and failed transactions.

Takenos, a LATAM fintech building modern infrastructure for cross-border workers, doubled approval rates after migrating to Coinflow and sustained 28% monthly user growth across new markets and verticals. Real-time stablecoin settlement replaced multi-day clearing cycles, and embedded fraud and chargeback indemnification removed risk that previously capped expansion.

Marketplaces with global seller networks face a different version of the same problem. Sellers expect access to earnings the moment a sale completes, not three days later. Standard T+2 or T+3 settlement creates working capital pressure for sellers and stalls inventory turnover for the platform.

Stablecoin rails collapse that gap. Sellers get same-transaction access to funds, platforms reduce reconciliation overhead, and the entire marketplace flywheel speeds up. In every one of these use cases, end users never interact with crypto. They pay and receive local currency. Blockchain does its work invisibly, in the middle.

When evaluating blockchain cross-border payment infrastructure, the technology is the easy part. What separates production-ready providers from experiments is everything wrapped around the rails. A few criteria worth weighting heavily:

Stablecoin settlement only helps if you can also accept local payment methods on the front end and deliver local currency on the back end. Coverage across 170+ local methods turns blockchain rails into a complete corridor solution.

AML, KYC, sanctions screening, and Travel Rule obligations are not optional. Working with a licensed partner, such as Coinflow, which operates as a Polish-registered VASP and maintains SOC 2 and PCI DSS Service Provider Level 1 compliance, transfers most of that burden off your roadmap.

Blockchain settlement is final, but the pay-in side still carries dispute risk. Indemnification turns that exposure into a fixed cost rather than a variable one.

Multi-rail orchestration matters more than any individual rail. The right platform routes each transaction over the optimal rail, blockchain or otherwise, behind one integration.

For the platforms building the next layer of global commerce, blockchain cross-border payments work best when they disappear into the infrastructure.

Coinflow's stablecoin-powered rails deliver instant settlement, 170+ local pay-in and payout methods, embedded AML and KYC, and full chargeback indemnification through a single API. Pay-in, settlement, FX, and payout move as one continuous chain instead of four disconnected vendors.

That means software platforms, fintechs, marketplaces, gaming companies, and remittance providers can offer their customers fast, predictable, global money movement without building blockchain expertise in-house and without exposing end users to crypto complexity.

Talk to the Coinflow team to see what a phased rollout of blockchain rails could look like for your highest-friction corridors.

John Thomas Lang is Head of Marketing at Coinflow and a two-time $1B-unicorn brand builder known for turning early-stage companies into high-growth, category-defining businesses.

Remittance

Choosing a payment gateway service for global growth? Compare Coinflow, Stripe, Adyen, Checkout.com, and Braintree on settlement, payouts, and risk coverage.

Cross Border

Global compliance now costs financial institutions $206B a year. Here's how to navigate AML, data, licensing, sanctions, and tax across markets without losing speed.

Fintech

Real-time payments are projected to hit 22% of global transaction volume by 2028. Here's how marketplaces, e-commerce, gaming, payroll, remittance, and fintech platforms are using instant settlement to drive real business outcomes.