Marketplaces

How to Offer Instant Payouts to Your Marketplace Sellers

You can't pay out money you don't have yet. The real fix for instant payouts starts upstream, at settlement.

Marketplace reconciliation breaks when money moves through disconnected systems. Learn how today’s top marketplaces automate reconciliation by design.

Payment reconciliation sounds straightforward. Money comes in. Money goes out. You make sure the numbers line up.

For marketplaces, that mental model breaks almost immediately.

That’s because marketplaces don’t move money once. They move money between people, across systems, over time, and every step introduces opportunities for things to drift out of sync.

When reconciliation becomes painful, it’s rarely because the finance team isn’t working hard enough. It’s because the underlying payment flows were never designed to reconcile cleanly in the first place.

Let’s unpack why reconciliation gets so messy for marketplaces and what “automation” actually means when it works.

In your typical ecommerce business, one order usually maps to one payment and one revenue entry. Simple enough.

In a marketplace, a single buyer transaction sets off a chain reaction:

Each of those events can occur at different times, in different systems, with different identifiers. The more sellers, payout methods, geographies, and payment rails you add, the harder it gets to keep everything aligned.

This is why reconciliation issues don’t show up all at once. They creep in slowly, one timing difference here, one missing reference ID there, until someone eventually asks: “Why doesn’t this payout match this order?”

And suddenly everyone is digging.

Marketplaces deal in multi-party money movement by default. A single buyer payment might need to be split between sellers, platform fees, taxes, reserves, and scheduled payouts.

Those flows rarely settle at the same time. Authorization, capture, settlement, and payout all happen on different clocks. Some fees are deducted before settlement. Others after. The result is a constant stream of “almost right” numbers that don’t quite line up.

Most marketplaces rely on a patchwork of tools that were never designed to act as a single system.

Each system uses different transaction IDs, different settlement logic, and different reporting formats. None of them has the full picture of how money actually moved end to end.

So teams fall back on spreadsheets. Not because they want to, but because there’s no other way to reconcile across disconnected systems.

Marketplace money is almost always in motion. Funds sit in rolling reserves, batch files, or net settlement reports for days or weeks.

During that time, the system says the money exists, but no one can clearly see where it is or when it will be available. That gap is where most reconciliation issues start, long before accounting ever gets involved.

Spreadsheets work…until they don’t.

As transaction volume grows and payouts become more frequent, manual reconciliation hits hard limits. Human review can’t keep up. Monthly closes turn into forensic investigations. Finance teams receive inconsistent data too late to prevent downstream issues.

And when sellers start asking about missing payouts or incorrect balances, reconciliation stops being a back-office problem. It becomes a trust problem.

A lot of tools promise reconciliation automation by “matching transactions faster.” That’s not the real problem.

Marketplaces don’t need better matching. They need fewer mismatches.

True reconciliation automation comes from having a single, consistent view of the entire payment lifecycle — from buyer charge to seller payout — tied together with shared transaction data.

When the system knows how money moved because it was designed that way, reconciliation becomes largely automatic by default.

Clean reconciliation doesn’t happen downstream. It’s designed upstream.

When pay-ins and payouts live on separate infrastructure, reconciliation is guaranteed to be messy. When settlement timing is opaque, teams are forced to infer what happened instead of knowing it.

Marketplaces run into these issues because most traditional payment providers optimize for acceptance, not multi-party financial accuracy. The burden of stitching everything together is pushed onto operations and finance teams later.

That’s the opposite of automation.

When pay-ins and payouts live in different systems, every handoff introduces new discrepancies.

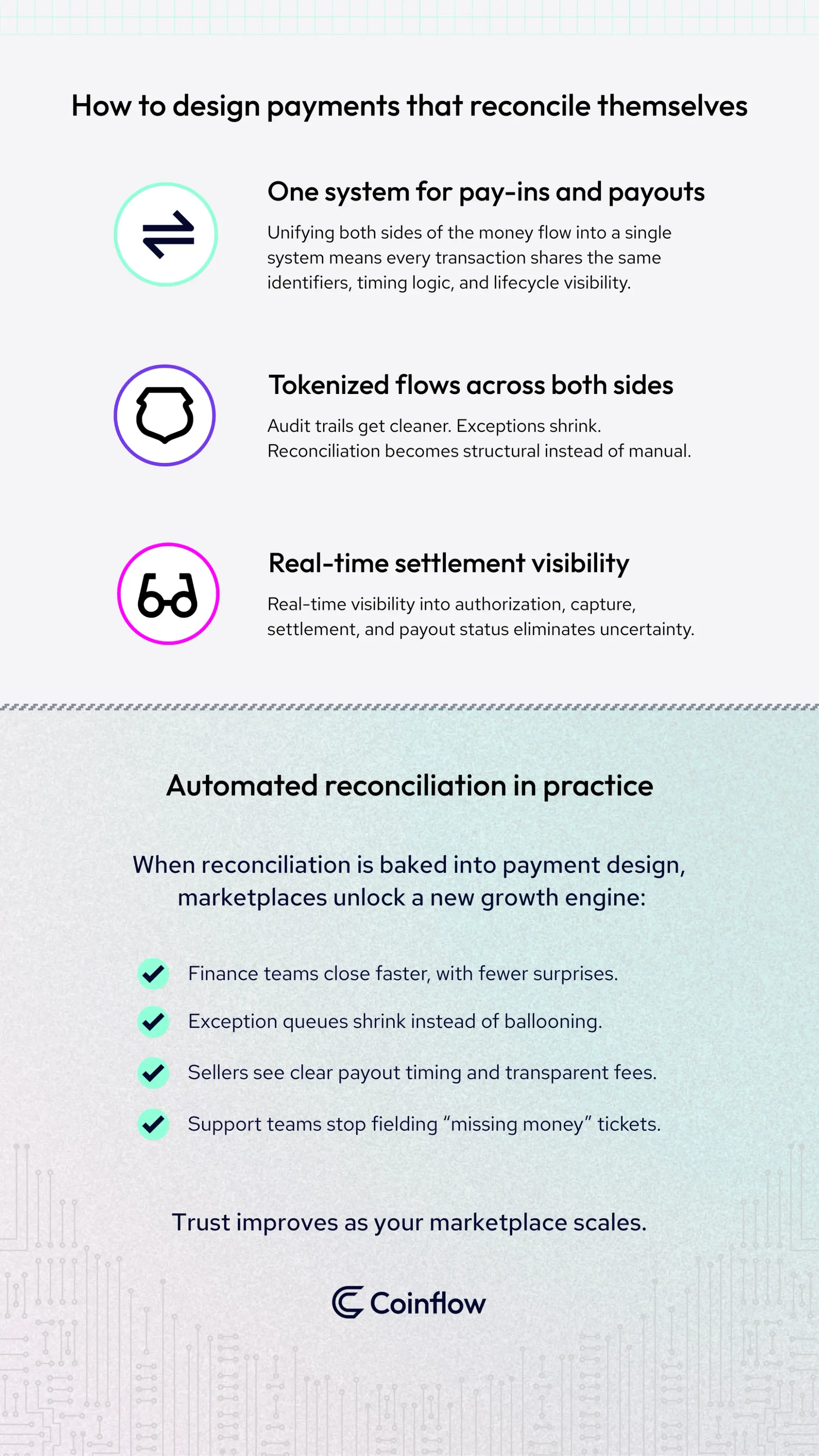

Unifying both sides of the money flow into a single system means every transaction shares the same identifiers, timing logic, and lifecycle visibility. There’s no need to reconcile across providers because there’s nothing to stitch together.

Tokenization is often framed as a security feature, but it’s also a reconciliation unlock.

When both buyer payments and seller payouts are tokenized, transaction identity stays consistent across repeats, retries, and recurring flows. Audit trails get cleaner. Exceptions shrink. Reconciliation becomes structural instead of manual.

One of the most common support tickets marketplaces get is painfully simple: “Where is my money?”

Real-time visibility into authorization, capture, settlement, and payout status eliminates that uncertainty. Teams can spot mismatches early, before they cascade into accounting issues or seller disputes.

When reconciliation is baked into payment design, the effects ripple across the business.

Most importantly, trust improves (internally and externally) as the marketplace scales.

Marketplace reconciliation doesn’t break because teams aren’t working hard enough. It breaks because money moves through too many disconnected systems.

When payments infrastructure is designed specifically for marketplaces—unifying pay-ins, payouts, tokenization, and settlement visibility—reconciliation stops being a constant cleanup exercise and becomes largely automatic by design.

If reconciliation still feels like cleanup work, it’s usually a sign the payments layer needs attention. Talk to our team to walk through how your money actually moves—and where automation can remove friction. Coinflow helps marketplaces simplify money movement at the source, so reconciliation stays clean as you scale.

Because a single buyer payment triggers a chain of downstream events: platform fees, seller balance updates, reserves, settlement, and potential chargebacks, each tracked in different systems on different timelines. Traditional ecommerce maps one order to one payment. Marketplaces map one order to many financial events, and that's where things drift out of sync.

In most cases, the root cause of reconciliation problems is that pay-ins and payouts live on separate systems with different identifiers and timing. Layering automation on top of fragmented infrastructure can help, but the gains tend to be incremental. The biggest improvement comes from unifying both sides of the money flow on shared infrastructure, which is a more foundational change.

Delayed settlement creates an "in transit" period where money exists but can't be verified, the most common source of reconciliation exceptions. When settlement happens in real time, you always know exactly where funds are, eliminating the guesswork that drives manual investigation and seller support tickets.

Reconciliation software tries to match data after the fact, across fragmented systems. Reconciliation by design means payment infrastructure is built so that every transaction carries a consistent ID from buyer charge to seller payout, and settlement timing is transparent, so there's little to reconcile in the first place.

John Thomas Lang is Head of Marketing at Coinflow and a two-time $1B-unicorn brand builder known for turning early-stage companies into high-growth, category-defining businesses.

Marketplaces

You can't pay out money you don't have yet. The real fix for instant payouts starts upstream, at settlement.

Fintech

Real-time payments are projected to hit 22% of global transaction volume by 2028. Here's how marketplaces, e-commerce, gaming, payroll, remittance, and fintech platforms are using instant settlement to drive real business outcomes.

Marketplaces

How do you turn liquidity into growth? For Courtyard.io, the answer was clear: give sellers instant access to their funds and watch growth happen.